How Cigna Remains at the Top of the Health Insurance Food Chain

The health insurance industry has received a lot of backlash over its managed care practices that bog down providers with pre-authorizations and rampant medical claim denials. The rise in medical benefits ratios (MBRs) driven by Medicare Advantage plans have squeezed margins for major health insurance providers like Humana Inc. (NYSE: HUM), UnitedHealth Group Inc. (NYSE: UNH), and CVS Health Co. (NYSE: CVS). However, one major insurer saw the writing on the wall early on and divested its Medicare Advantage business to protect its margins.

The Cigna Group Inc. (NYSE: CI) is at the top of the health insurer food chain. The company has demonstrated its foresight and agility to quickly navigate the changing landscape of the healthcare industry within the medical sector.

How Cigna Masterfully Navigates the Trends in Healthcare

Cigna has skillfully bobbed and weaved its way around the healthcare landscape, jumping on trends ahead of time and sidestepping potholes along the way. They jump-started their Medicare Advantage (MA) gravy train in 2011, acquiring HealthSpring Inc. for $3.8 billion to pump up its MA membership from 46,000 to 400,000 members.

For over a decade, Cigna scored billions from MA until their spider senses kicked in. They saw the writing on the wall and exited when the inpatient utilization rates started climbing, selling its Medicare Advantage business (along with its Medicare Part D and Cigna Supplemental Benefits business) for $3.3 billion to Health Care Service Corporation (a major non-profit health insurer offering Blue Cross Blue Shield plans) in January of 2024. This is why the rumors of Cigna acquiring Humana made no sense, as they would be reentering the MA market, which it had just exited.

Cigna entered the lucrative pharmacy benefits management (PBM) business with its $67 billion acquisition of Express Scripts in December 2018. By doing so, it also acquired EviCore, a third-party medical benefits management (MBM) and utilization firm. EviCore is often outsourced by insurance carriers to use data analytics and artificial intelligence (AI) powered intellipath solutions to handle pre-authorization and claims management services, ensuring that treatments are medically necessary. Critics suggest EviCore is more of a way to outsource claim denials and shift responsibility onto a "neutral" third party. They are allegedly hired to automate claim denials and prolong the pre-authorization process in order to boost margins for their health insurance clients.

U.S. Healthcare Spending Surges 7.5% in 2023

According to the Centers for Medicare & Medicaid Services, its national health expenditure (NHE) data indicates healthcare spending in the United States grew 7.5% YoY in 2023 to $4.9 trillion or $14,570 per person, accounting for 17.6% of gross domestic product (GDP). Private health insurance spending rose 11.5% YoY. For 2023 to 2032, NHE is forecast to grow 5.6%, outpacing average GDP growth of 4.3%. Spending on healthcare will continue to outpace inflation.

This ensures healthcare is a growth industry, and metaphorically speaking, Cigna may be the nicest house in a rough neighborhood.

Evernorth’s 50% Revenue Growth Drives Cigna’s 30% YoY Revenue Growth in Q3 2024

Cigna operates in two divisions: Evernorth Health Services and Cigna Healthcare. Evernorth operates PBM, specialty pharmacy, and care delivery and management (EviCore) business. Cigna Healthcare is an insurance business offering traditional health insurance plans. Cigna reported Q3 EPS of $7.51, beating analyst estimates by 28 cents. Revenues rose a whopping 30% YoY to $63.7 billion, crushing the $59.58 billion consensus estimates by over $4 billion.

Cigna’s Medical Care Ratio is Still One of the Highest in the Industry Compared to Peers

The medical care ratio (MCR) is the percentage of insurance premiums that are actually spent on medical care for its members. The higher the MCR, the less money the insurer makes. Cigna’s medical MCR was 82.8%, up from 80.5% in the prior year, but hugely better than competitor CVS’s MCR, which rose to 95.2% in its Q3 2024. Again, this illustrates how Cigna protected its MCR by selling its MA business while CVS's MCR surged to 95.2% (up from 85.7% the year before) by keeping its MA business, further demonstrating skillful agility by Cigna.

CI’s average consensus price target is $395.93, implying a 41.31% upside, and its highest analyst price target sits at $438.00. It has 13 analysts' Buy ratings and one Hold rating. The stock has a 1.69% short interest.

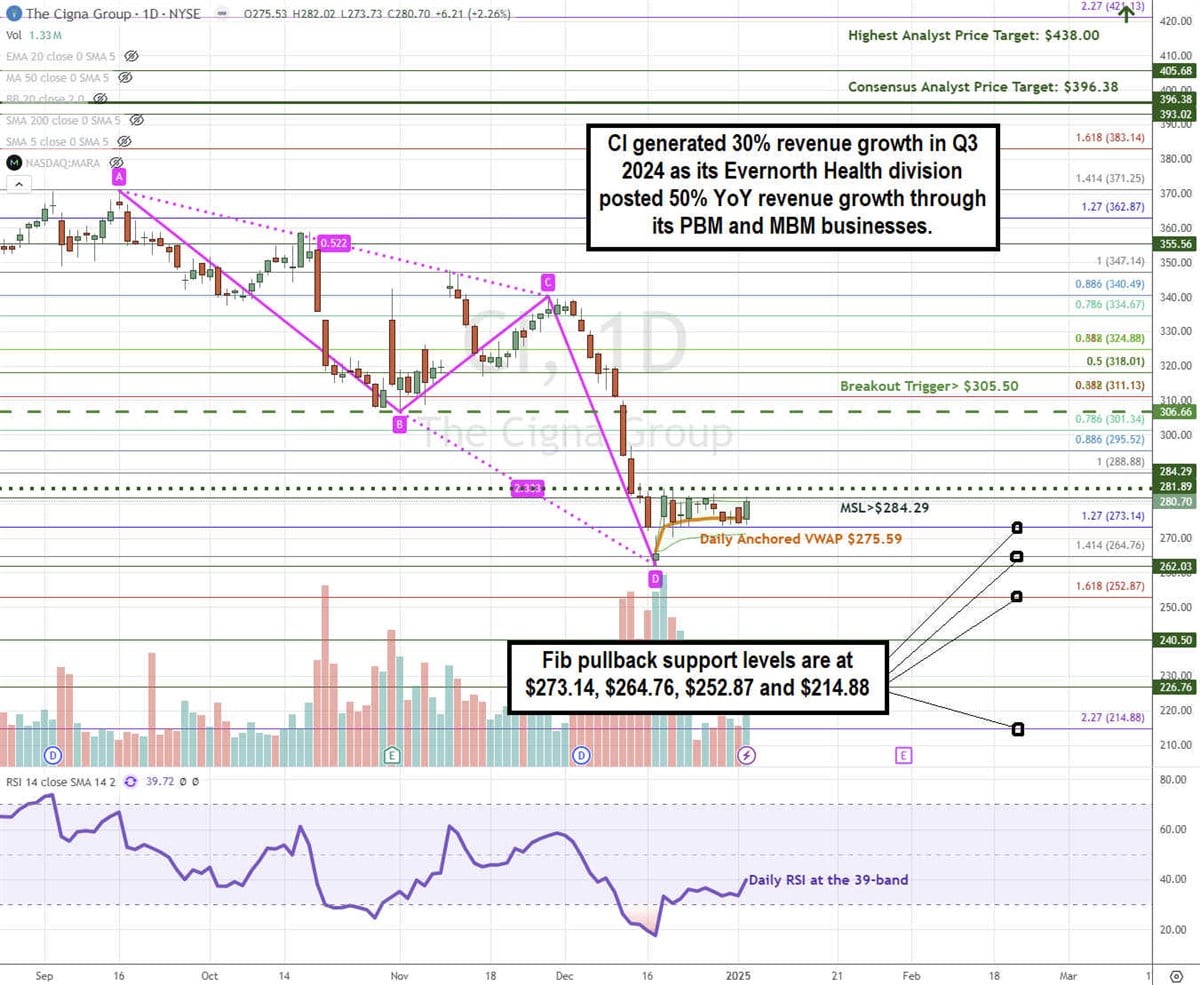

CI Forms a Potential ABCD Reversal Pattern

An ABCD reversal is a harmonic pattern comprised of four key points: A swing high, B bottom reversal, C peak, and D lower bottom reversal level. The reversal triggers when the stock bounces back up through point B.

CI formed the ABCD pattern comprised of a low and lower low that found support at the $273.14 Fib. The daily anchored VWAP is attempting to hold support at the $273.14 Fib as CI attempts to trigger a market structure low (MSL) buy signal above $284.29. The ABCD reversal breakout triggers above the $306.66 level. The daily RSI is starting to bounce at the 39-band. Fibonacci (Fib) pullback support levels are at $273.14, $264.76, $252.87, and $214.88.

Actionable Options Strategies: Bullish investors can consider using cash-secured puts at the Fib pullback support levels to buy the dip. If assigned the shares, writing covered calls at upside Fib levels executes a wheel strategy for income on top of its 2.00% dividend yield.

Learn more about CI