GitLab: Get In While It’s Down—Big Rebound Ahead

GitLab’s (NASDAQ: GTLB) market may wallow near its early 2024 lows, but lower lows are unlikely, and a strong rebound lies ahead. The Q4 results and guidance for 2025 are the reason. However, the strong results and outlook weren’t the cause.

The market had set a high bar driven by ramping demand for AI software, which created a no-win situation for the stock price; no result short of a mind-boggling, NVIDIA (NASDAQ: NVDA)-like performance would have been sufficient to catalyze a rally.

The critical takeaway from the guidance is that this company forecasts another year of solid 20% growth, and the odds are high that the guidance is cautious. GitLab has outperformed every quarter since its IPO and is unlikely to break the streak due to increasing demand for AI products and services.

GitLab’s Strength Overshadowed by Market Forecasts

GitLab had a solid Q4, showing increasing demand and leverage with existing clients, which suggests the 2025 guidance is cautious. The company reported $211.4 million in net revenue for Q4, up nearly 30% and 250 basis points better than expected on an increased client count and deepening penetration. Clients contributing $5,000 in ARR grew by 15%, but the more prominent clients, contributing more significant $100K and $1M in annual ARR, grew by 29% and 28%, while retention came in at 123%.

Operating leverage is also growing. The company continues to post GAAP losses, but losses are narrowing, adjusted profitability is improving, and free cash flow conversion is impressive. The company widened its adjusted operating margin by 1000 basis points to 18%, generating $63.2 million in operating cash flow with a 98% free cash flow conversion. Free cash flow is up more than 150% yearly and is expected to grow in 2025.

The guidance is shy of the consensus reported by MarketBeat but no less potent. The company forecasted 23% revenue growth at the top line and is likely cautious given the strength of large client growth, penetration gains, and the 40% increase in RPO. Outperformance is the likely scenario; the question is how much.

The Analysts Affirm GitLab’s Moderate Buy Rating and Upside Potential

The analysts’ response to GitLab’s results and guidance is a mix of reduced and reiterated price targets that align with the consensus estimate. It is a 30% upside from critical support targets when reached. The takeaway from the commentary is that GitLab’s results weren’t all that impressive, but the demand outlook has stabilized, and the long-term forecasts are unchanged.

The long-term estimates include a 20% top-line compounded annual growth rate for at least the next eight years with a widening margin. Earnings are expected to grow at a rough 30% CAGR for the same period.

Institutional activity aligns with the outlook for higher share prices over time. Not only do the institutions own more than 95% of the stock, but their buying activity ramped to a multiyear high in Q1 2025. Institutional buying in Q1 hit a record high, more than doubled the selling pace, and netted a half-billion dollars worth of shares, about 6.5% of the market cap, with the stock trading near $58.

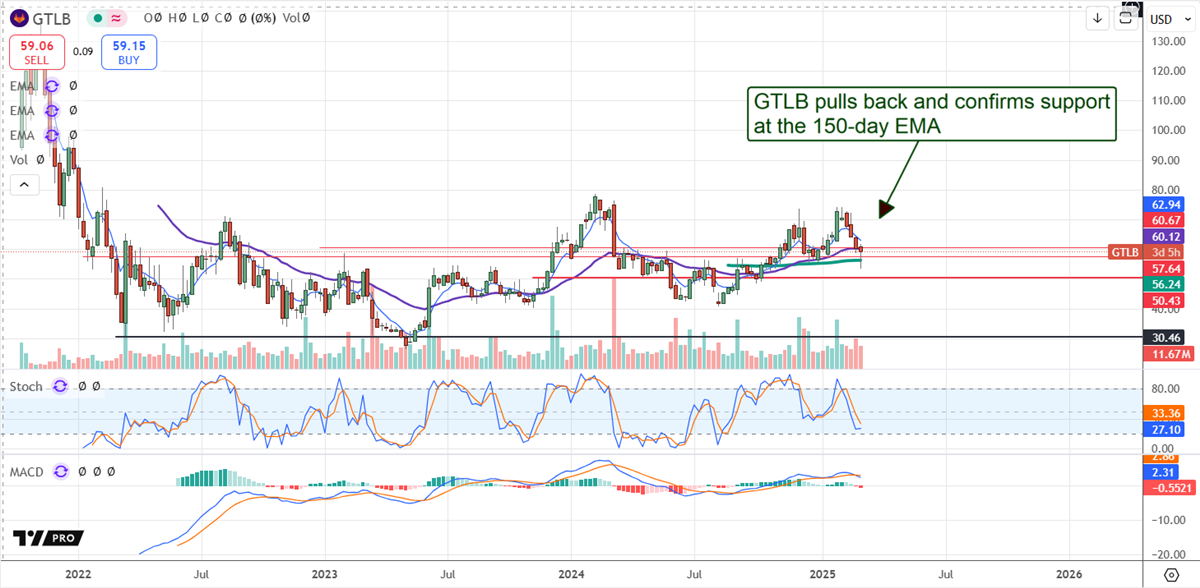

GitLab Confirms Support at a Critical Level; Sets Up for 2025 Rebound

GitLab’s price action fell the day before the release and opened with a gap following, but lower lows are unlikely. The market quickly rebounded from its early low to confirm support at the 150-day EMA, an indicator of long-term investor support, including institutions and analysts' followers. The likely scenario is that support will remain solid in the low to mid-$50s, causing this market to move sideways until traction is regained.